According to the Roadmap for a Renewable Future Report (REmap) released by the International Renewable Energy Agency (IRENA) , great strides have been made to increase renewables in the power sector, which is on track to generate roughly 30 per cent of the world’s electricity by 2030 (up from 23 per cent today). There is also great potential to increase renewables in transport, buildings and industry, but these sectors are currently lagging behind.

Doubling the share of renewables in the global energy mix by 2030 can save up to USD 4.2 trillion annually by 2030 thanks to avoided expenditures on air pollution and climate change. It would also create more jobs, boost economic growth, save millions of lives annually through reduced air pollution, and – when coupled with greater energy efficiency – put the world on track to keep the rise of temperatures within 2°C, in line with the Paris Agreement.

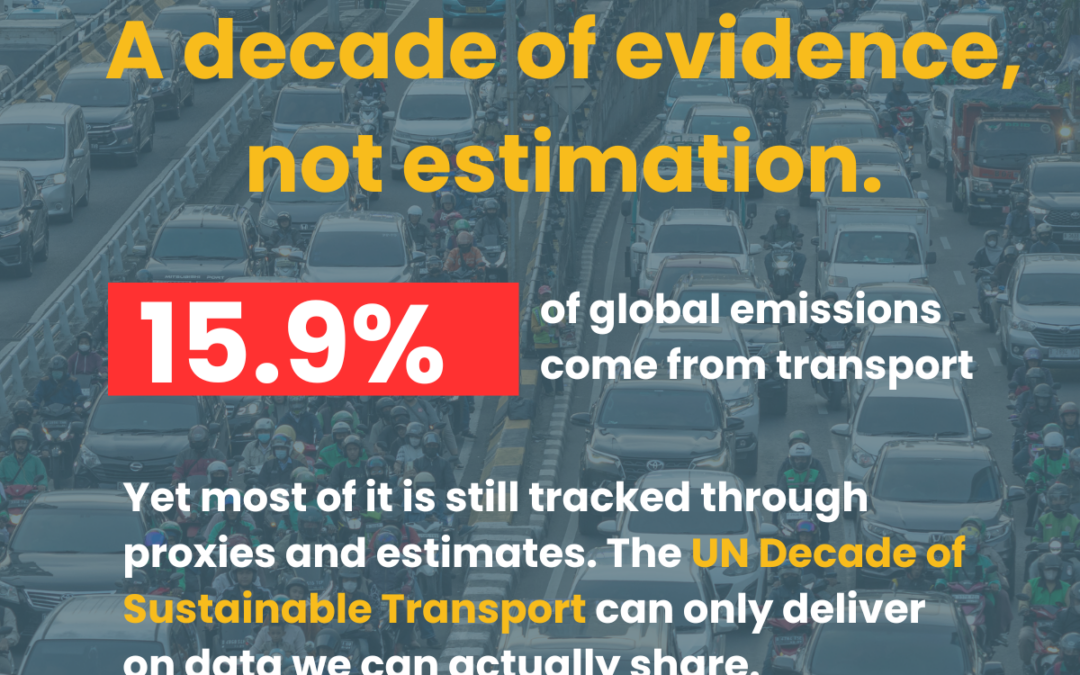

The transport sector now accounts for about 23% (7.3 Gt) of annual global energy-related CO2 emissions (32 Gt). Oil is expected to remain the dominant transport fuel in the coming years, and thus must be offset by a rapid decarbonisation of fuels and scaling up of renewable energy in the transport sector. The report concludes that transport could see five-fold growth through an increased uptake of liquid biofuels and rapid growth in electricity-based mobility. Although transport is the sector with the smallest share of renewables currently, it could grow five-fold however if opportunities in biofuels and electric mobility are captured.

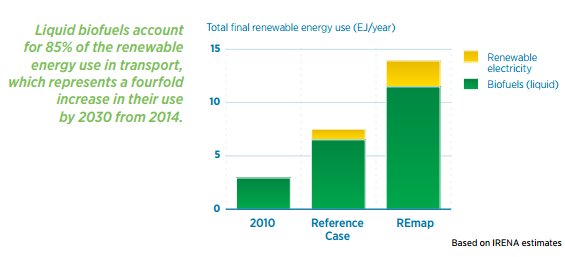

In the business as usual (the Reference Case in this report) Reference Case, global transport energy demand would reaches 130 EJ in 2030, compared with 92 EJ in 2010, an increase of about 40%. Total demand for electricity in transport would reach 3 EJ in the Reference Case, just under a doubling over today’s level. With the REmap Options the sector could significantly increase its share of electricity use to about 5.4 EJ, more than 40% of which would be generated by renewables.

• Reference Case: Deployment based on each country’s plans and policies today (BAU scenario)

• REmap Options: The deployment potential of additional renewable energy technologies by 2030 on top of today’s existing policies

• Doubling Options: Additional renewable energy deployment combined with deeper structural changes

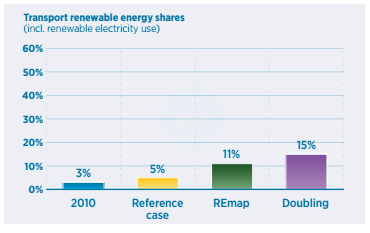

Figure 1: Transport renewable energy shares

As shown in Figure 1, renewables represented only 3% of total final energy consumption (TFEC) in transport in 2010 and about 0.2% from renewable energy through electric mobility. In the Reference Case, that total would rise to 5%, and with the REmap Options to 11%. The renewable energy breakdown in 2030 shows considerable differences across countries. In countries where electrified railways and public transportation are common, such as in some European countries, electric mobility accounts for the largest share of renewables. In the United States, Brazil and in some European countries conventional biogasoline* (incl. ethanol) dominates the mix. With the REmap Options, Sweden, Ethiopia, and Brazil would have the highest share of renewables overall, at more than 30%, with Denmark, Germany, and France and Indonesia all between 20% and 25%.

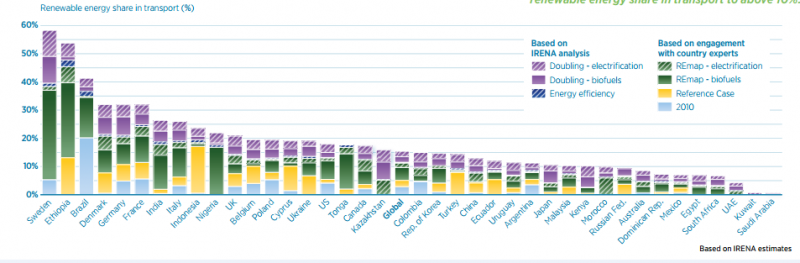

Liquid biofuels must continue to play an important role, particularly as other low-carbon options are limited in their ability to meet demand for long-haul and heavy transport, aviation and shipping. Liquid biofuels are also a way to diversify energy sources for importers. Brazil is expected to continue to focus on liquid biofuels and further develop deployment potential. Both Denmark and Sweden have great potential for advanced liquid biofuels and biodiesel (including freight) beyond their Reference Cases. In addition to this potential, a large deployment of EVs is expected. All countries have a significant deployment potential simply because the base level is very low. As shown in Figure 2, more than half of all REmap countries can raise the renewable energy share in transport to above 10%.

Figure 2: Share of renewable energy in transport energy use in Remap countries, 2010-2030

In China, the government offers various incentives for the deployment of alternative-energy vehicles and has set a target of 5 million alternative energy vehicles by 2020. France, Germany, Norway, the Netherlands and the United States also have electric mobility targets, but overall the growth in EVs has been slow. According to the REmap findings, up to 10% of the total global vehicle fleet will be either EVs or plug-in hybrids by 2030 if all REmap Options identified in the 40 countries are implemented. This would constitute 160 million vehicles in the total vehicle stock in 2030. Realizing this potential would require yearly sales to reach 10 million, up from just around 0.5 million last year (IRENA, 2015f). In addition, electric two and three wheelers, used largely in Asia, would number 900 million, up from 500 million expected in the Reference Case.

Shown in Figure 3, in the Reference Case, global transport energy demand would reaches 130 EJ in 2030, compared with 92 EJ in 2010, an increase of about 40%. Total demand for electricity in transport would reach 3 EJ in the Reference Case, just under a doubling over today’s level. Total liquid biofuel demand would reach roughly four times the level in 2014 (128 billion litres).

Figure 3: Total final renewable energy use in transport, 2010 – 2030

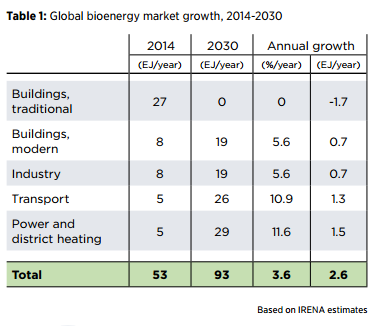

Bioenergy will continue to be the largest source of renewable energy in 2030 with all REmap Options and Doubling Options implemented, accounting for half of the total global renewable energy use. As shown in Table 1, technology and policy challenges to realising this potential are significant. Different types of bioenergy feedstock will be required for various applications. In transport, a total of 500 billion litres liquid biofuel will be required annually. Given the recent investment trends, meeting this demand will be a challenge, in particular scaling up of cellulosic biogasoline production to commercial levels, which is today limited.

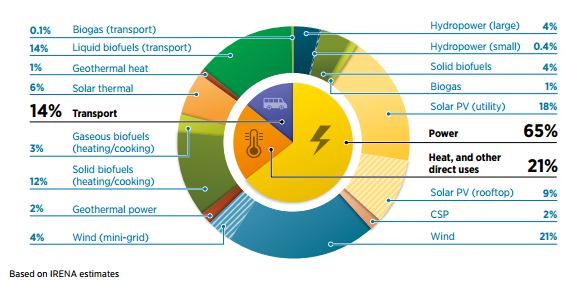

Figure 4 below shows that 14% of CO2 emission could be avoided by the use of renewable energy in the transport sector by 2030, ranking no. 3 after the power sector (65%) and heating (21%).

Figure 4: Avoided CO2 emissions by sector and technology with Remap Options, 2030.

Transport could see five-fold growth through an increased uptake of liquid biofuels and rapid growth in electricity-based mobility. Transport is the sector with the smallest share of renewables; this could grow five-fold however if opportunities in biofuels and electric mobility are captured.

For the full report, please see here.

The SLoCaT Partnership has also released a report on decarbonising fuel in the transport sector through renewable energy as part of the series of knowledge products under the Paris Process and Mobility and Climate. The report is available here.